4 July 2022

By Liew Jia Teng and Cheryl Poo

SO far, 2022 has been a bad year for most stock pickers. At a time when the world is still learning to live with Covid-19 and adapt to the new norms, many countries have seen the highest inflation rates in decades as a result of supply shortages and strong consumer demand.

Russia’s invasion of Ukraine in February not only created Europe’s largest refugee crisis since World War II, but also caused food shortages around the globe. Ukraine is often described as being the “breadbasket of Europe” as it is among the world’s top agricultural producers and exporters.

China — the world’s factory — has imposed a zero-Covid policy to curb the spread of infections, but the extreme measures have severely disrupted global supply chains.

In mid-June, the US Federal Reserve raised its benchmark interest rate by 75 basis points (bps), its most aggressive hike since 1994. This took the Fed funds rate to a range of between 1.5% and 1.75%, the highest since just before the pandemic began in March 2020.

In a move to tame the US’ fastest inflation rate in four decades, Fed chairman Jerome Powell expects to see another increase of 50bps or 75bps at the central bank’s meeting in July.

Against the backdrop of inflationary pressure and supply chain disruptions, the US seems to be willing to sacrifice economic growth, while the Fed is no longer pumping temporary liquidity into Wall Street like it did in 2020.

As the US appears to be heading towards a hard landing, corporate observers point out that it could lead to a recession akin to the 1970s stagflation, which eventually led to the “Volcker Recession”.

Notably, the Fed under Paul Volcker raised interest rates above 19% to get inflation down, precipitating a steep economic downturn. His tough medicine led to not one, but two, recessions before prices finally stabilised.

Amid US recession fears, what should investors do? What are the fund managers’ trading and investment strategies? Given the current weak market sentiment, do they see another once-in-a-decade opportunity for bottom fishing?

Don’t rush in, as market cycles are shorter

The market experts whom The Edge spoke to believe now is not the time for investors to rush into the market. According to Tradeview Capital Sdn Bhd CEO Ng Zhu Hann, investors should take a more prudent approach towards investing and nibble at tranches.

“Do not rush in, and make sure to prolong your investment horizon. Market cycles these days are shorter than before. Instead of the usual 10 years, it is now five to seven years on average. So, if investors are prepared to take a longer-term view, then entering the market at different levels provides a good margin of safety,” he says.

Ng acknowledges that it is never easy to invest in the stock market in the face of uncertainty. During a bull market, when sentiments are good, everyone seems to be a professional investor. However, the best investors are those who can navigate well during a bear market.

“In fact, the best time to buy is always when market sentiment is down. Time is your best ally. With a prolonged investment horizon, each market downturn is merely a blip in the grander scheme of things,” he stresses.

“No one can time the bottom with 100% accuracy, not even professionals. If there is a wonderful company you have always wanted to buy into, but the valuations were stretched in the past, you could possibly start looking now. I believe better days are ahead for the local stock market once the political uncertainty clears up.”

Fortress Capital Asset Management (M) Sdn Bhd investment director Chua Zhu Lian agrees that nobody can time the market accurately and consistently, as the world has too many black swan events, such as pandemics and wars, which make it impossible to predict market movements. “I think people shouldn’t be in the game of selecting specific equities for their investments, unless they are ready to face a decline in their investments by more than 50% without losing their peace of mind,” he warns.

Chua points out that the best strategy would be dollar cost averaging, which means investing smaller amounts over a period of time in an effort to reduce the impact of volatility on the overall purchase. “Most people would outperform their peers just by deploying the dollar cost averaging strategy on passive investments such as exchange-traded funds (ETFs),” he says.

Areca Capital Sdn Bhd CEO Danny Wong Teck Meng opines that for investors, the key is to look at the long term. With a longer-term view, he believes now is the time to look at stocks’ fundamentals.

“I don’t think stocks are very cheap right now. There won’t be bottom fishing like back in the day. Maybe we have pulled back about 1.5 standard deviation below the long-term mean, but not two yet. Second, in a rising interest rate environment amid a stubbornly high inflation rate, putting money in low earning instruments may not be a wise move,” he cautions.

“My advice is that investors look at equities that are not very aggressive or stocks that can form a diversified portfolio, where a certain percentage of it comprises growth stocks, like technology and semiconductor, as well as a certain percentage of dividend-yielding stocks and real estate investment trusts (REITs). This will help counter the high inflation risk.”

Will the FBM KLCI fall into bear territory?

Global stock markets fell sharply due to fears that a more aggressive rate hike by the Fed could lead to a US recession.

Year to date, the Nasdaq Composite Index has declined 31%, while the S&P 500 fell 23%. The FBM KLCI, however, has only declined 8%. While US stocks are clearly in a bear market, it appears that Malaysian stocks have yet to fall into bear territory.

The FBM KLCI has slipped 15% from its peak of 1,685 points in December 2020. In general, a 20% fall from the peak would constitute a bear market, whereas a 10% decline would be a correction.

Tradeview’s Ng says, “Our local stock market appears to be more resilient because the FBM KLCI did not make a new high and barely returned to pre-Covid levels of above 1,600 points. Hence, there is not much room to fall compared with markets in the US and Europe, where the stock markets had rallied significantly over the past two years due to expansionary monetary policies.”

Furthermore, he says, the FBM KLCI has always been a low beta market, averaging at 0.51 times versus the S&P 500, which means it is less sensitive to price rallies and plunges. Besides, being a commodity-producing nation, Malaysia is supposedly a beneficiary of the commodity price shocks that are roiling markets around the world.

“These factors together ought to have made the FBM KLCI more resilient to the recent downswing. Personally, I am of the view that it is highly unlikely for our local stock market to enter bear market territory [20% plunge]. The risk factor for our country primarily stems from political instability, policy continuity concerns and high debt levels due to insufficient government revenue versus expenditure outflow,” says Ng.

Fortress Capital’s Chua agrees that the local stock market is unlikely to decline by the same quantum as US equities as it was already underperforming the US markets. Nevertheless, there is still the risk of a further decline, given the continuous withdrawal of foreign funds amid interest rate hikes in the US.

“If the default rates in the banking sector pick up significantly, or if there are unexpected political shockwaves, these may lead to a more severe decline in the Malaysian market,” he points out.

When the market crashes

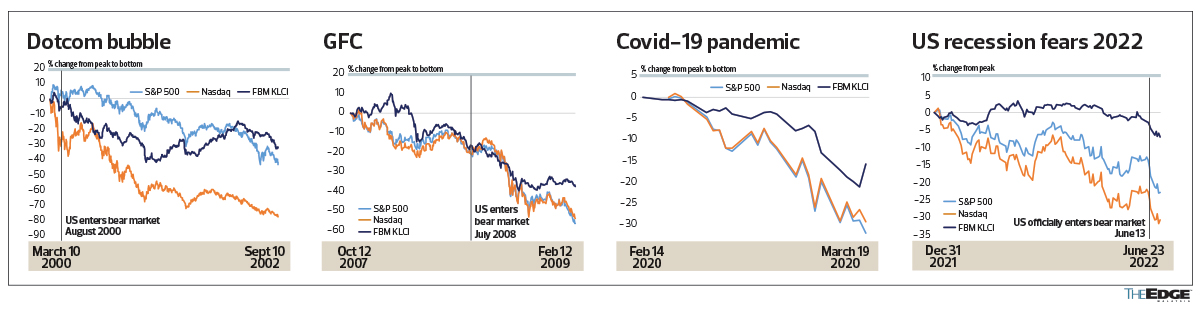

There have been a few major market crashes in the past two decades. First, it was the dotcom bubble in 2000/01. Then came the 2008 global financial crisis. And the most recent was during the outbreak of Covid-19 two years ago.

A quick compilation by The Edge shows that from peak to trough, the FBM KLCI fell 41% during the dotcom bubble, which was in line with the 43% drop of the S&P 500, but smaller than the Nasdaq’s 77% decline.

During the global financial crisis, the FBM KLCI fell 38%, which was less severe than the more than 50% drop of the S&P 500 and Nasdaq. Similarly, during the bear market amid the Covid-19 outbreak in 2020, the 16% drop of the FBM KLCI was less significant than the 30% decline of the S&P 500 and Nasdaq.

So, what is the main difference between the current recession fears and in previous crises? The short answer is the lack of liquidity as a result of monetary tightening to tame high inflation.

Tradeview’s Ng observes that negative headlines have dominated the news cycle of late and no doubt these have dampened investor sentiment globally.

“As recently as one year ago, many market strategists appeared to have a consensus that there will be a strong recovery in the global economy as we emerge from the pandemic. However, this has not happened of late because of inflation,” he says.

Ng goes on to say that the extremely high inflation — which was in part due to supply chain disruptions and pent-up demand following the reopening of economies, coupled with the after-effects of loose monetary policies — have made central banks around the world more hawkish.

“Hiking interest rates and tapering their bond buying will significantly reduce market liquidity and this will have an impact across all asset classes. I strongly believe all economic crises or market crashes differ in root cause. The only thing in common is where the valuation of asset classes outpaces fundamentals relative to interest rates, then a correction or mean reversion would occur,” he says.

Fortress Capital’s Chua says a crisis leading to a sharp decline is usually caused by largely unpredictable adverse shocks.

“However, in this crisis, most major shock factors are cards that have already been dealt and opened, instead of wild cards. The market crashes were also smoother compared to the previous crises, giving the world a breather from the more forgiving circumstances of Covid that normally will not be available under a BAU (business as usual) operating environment,” he adds.

Not a recession yet

UOB Malaysia senior economist Julia Goh insists that her research firm’s base case does not include a recession yet and its updated quarterly forecasts anticipate slower growth and higher inflation in the major economies.

“However, it has been a volatile quarter for global markets, where key assets were sold aggressively across the board. There were widespread and elevated fears of recession or stagflation amid a further rise in inflation,” she says.

“The Ukraine crisis is now more protracted, so the world will have to deal with the adverse fallout on prices and growth. The world is also dealing with a weaker China economy, which adds further headwinds to global growth, as well as the Fed accelerating its rate hike cycle. These multiple headwinds will pose more challenges and risks for emerging markets, including Malaysia.”

If a recession does occur, she believes Malaysia will be affected via trade, investment or financial linkages. “The extent of fallout on markets will also depend on the degree of the recession — mild or severe, synchronised across multiple countries or not. A milder technical recession equivalent to two straight quarters of GDP declines would be less worrying than a longer and deeper recession that extends beyond two quarters across many developed countries,” says Goh.

On a positive note, following a long bull run in the US markets since 2009, some see a silver lining in a recession, if it happens.

Given that a strong bull run may cause equities to be overvalued, a short-term recession could actually help slow down inflation and, hence, allow assets to be fairly priced.

Areca Capital’s Wong believes that if there is a prolonged recession in developed markets, the demand from developed markets and exports from developing markets will be affected. Therefore, Malaysian sectors such as manufacturing and exports will be impacted, which will then have a knock-on effect on banking, where loan growth will slow and affect consumer spending.

“All this happens in a prolonged recession. Having said that, I do not think a recession will happen. Even if it does, it will only be a technical recession and for a very brief period only,” he says.

Ng also does not think a full-blown prolonged recession will happen, but rather a “profit recession”, or two consecutive quarters of earnings decline, is more likely.

“I foresee a short-term down-market cycle. In the case of the global stock market [not Malaysia], indeed it has rallied in the past two years. I am of the view that a market correction, not a crash, is timely considering how valuations have far exceeded the underlying intrinsic value of asset classes, be it equities, commodities or bonds,” he says.

To a large extent, says Ng, a correction helps restore sanity and rationality to the market, and he believes that in the process, it will bring down inflationary pressure, as the market needs a cooling-off period in order to go further.

Meanwhile, Chua highlights that a recession will have an adverse impact on the earnings of the majority of corporations. Companies with highly inelastic pricing models will suffer the most, given the difficulty to pass on the higher cost of raw materials to customers.

“Sectors that are particularly vulnerable will be the airline and travel industry. Automotive may be sheltered because of domestic factors such as the overwhelming orders from the Sales and Service Tax break, while I believe semiconductor and cloud computing will continue to grow given the necessity for more and more IoT [Internet of Things devices] as the world progresses towards 5G adoption,” he says.

View Original Article